Law no. 234 of the 30th December 2021 (the 2022 Budget Law) postponed the main tax credits for businesses, including those for R&D, technological innovation, design, and those for the purchase of capital goods in industry 4.0. This article summarizes the main changes of the tax credits mentioned and the changes to Personal Income Tax (PIT) rates and deductions.

1. Tax credit for R&D, technological innovation, and other innovation activities (art.1, par. 45)

The tax credit for R&D activities has been extended from 2023 till 2031, for the tax period up to 31st December 2022, the tax credit for R&D activities is still recognized at the rate of 20% and within the annual ceiling of EUR 4 Million, but from the following tax period and up to the tax period up to 31st December 2031, the amount of the incentive decreases to 10% of the eligible expenses, and the annual ceiling of the credit increases to EUR 5 Million.

The tax credits for technological innovation, design, and aesthetic conception activities have been extended to 2025, while progressively reducing the rates. For the tax period in course as of 31st December 2023, is recognized at the rate of 10% and within the annual maximum limit of EUR 2 Million. As from the tax period in course until 31st December 2024 and until the tax period in course until 31st December 2025, the tax credit rate is reduced to 5% while the annual maximum limit of EUR 2 Million remains unchanged.

The tax credit for investments in 4.0 digital innovation projects or for projects aimed at achieving green transition objectives, for the tax period in progress as of 31st December 2022, 15% is confirmed within the annual maximum limit of EUR 2 Million, and then it is reduced to 10% for the tax period following the one in course on 31st December 2023, within the annual maximum limit of EUR 4 Million, and to 5% for the tax period following the ones in course from 31st December 2024 to 31st December 2025, within the annual maximum limit of EUR 4 Million.

2. Tax credit for investments in new capital assets 4.0 (art.1, par. 44)

For investments in new tangible assets included in Annex A of Law 232/2016, the article 1 (44) has extended the tax credit to the three-year period 2023-2025, the tax credit is recognized in the following measures:

- 20% of the cost for investments up to EUR 2,5 Million

- 10% of the cost for investments between EUR 2,5 Million and EUR 10 Million;

- 5% of the cost for investments between EUR 10 Million and EUR 20 Million.

About intangible assets included in Annex B of Law 232/2016, including expenses for services incurred in connection with the use of cloud computing solutions, the following percentages will apply, according to the year:

- from 16 November 2020 to 31st December 2023, the tax credit is granted at 20% of the cost, up to a maximum annual limit of eligible costs of EUR 1 Million;

- from 1st January 2024 to 31st December 2024, the tax credit is granted at 15% of the cost, up to an annual maximum of EUR 1 Million;

- from 1st January 2025 to 31st December 2025, the tax credit is granted at 10% of the cost, up to an annual maximum of EUR 1 Million.

In all cases, there is a 6-month window (until 30 June of the following year) if the conditions for the reservation are met by 31/12 of each year.

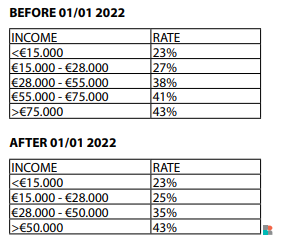

3. Changes to PIT rates and deductions

The Budget Law introduces PIT changes aimed to reduce the overall tax burden by:

- Amending the mechanism and magnitude of several PIT deductions

- Rewriting the tax brackets and applicable rates, as follows: